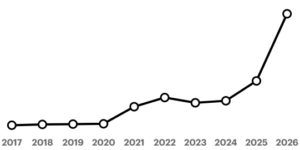

The global maritime order is currently undergoing a structural realignment driven by the intersection of aging tanker fleets and heightened regional instability. China’s shipbuilding sector is not merely experiencing a "wave of orders"; it is capturing a concentrated shift in capital allocation as shipowners hedge against the volatility of Middle Eastern energy corridors. This surge in Very Large Crude Carrier (VLCC) and Suezmax contracts represents a calculated response to a specific set of market constraints: a decade of underinvestment in tanker hulls, the exhaustion of South Korean yard capacity, and the specific risk profile of the Iranian conflict.

The Triple Constraint of Global Shipyard Capacity

To understand why China has become the primary beneficiary of current market tensions, one must analyze the capacity bottleneck defining the 2024-2027 delivery window. The global shipbuilding market operates under a tri-polar capacity constraint where China, South Korea, and Japan represent over 90% of global output.

- The LNG Displacement Factor: South Korean yards—traditionally the preferred choice for high-specification hulls—are currently near-maximum capacity due to an unprecedented backlog of Liquefied Natural Gas (LNG) carrier orders. This creates a "shadow vacancy" in China, which has aggressively expanded its drydock footprint to accommodate the overflow.

- Technological Parity and Cost Baselines: The historical "quality gap" between Chinese and Korean yards has narrowed significantly. Chinese yards now offer dual-fuel engine integration (LNG/Methanol ready) at a 10-15% price discount compared to their U.S. dollar-pegged Korean counterparts.

- The Steel-to-Hull Efficiency Ratio: China’s domestic steel production provides a vertical integration advantage. When geopolitical tension spikes, the cost of raw materials fluctuates; Chinese yards often absorb these fluctuations through state-backed credit lines, offering shipowners fixed-price contracts that are functionally impossible for private Korean firms to match.

The Mechanics of Conflict-Driven Demand

War in the Middle East, specifically involving Iranian maritime interests and the Red Sea corridor, does not just increase demand for oil; it alters the ton-mile multiplier. This is the fundamental unit of shipping demand, calculated by multiplying the volume of cargo by the distance traveled.

When the Suez Canal or the Strait of Hormuz becomes a high-risk zone, insurers hike premiums or outright deny coverage. Shipowners then reroute vessels around the Cape of Good Hope. This increases a standard voyage from the Persian Gulf to Rotterdam by roughly 40%, effectively removing 40% of the available fleet from the market due to longer transit times. The resulting "supply shock" in available hulls drives spot rates upward, providing shipowners with the liquidity required to place newbuild orders in Chinese yards.

The Shadow Fleet and the Replacement Cycle

A critical nuance often missed is the role of the "Shadow Fleet"—the aging, under-regulated vessels used to transport sanctioned oil. As Iran-related tensions escalate, the scrutiny on these vessels increases.

- Vessel Obsolescence: A significant portion of the current global VLCC fleet is approaching its 20-year limit.

- Regulatory Squeeze: The International Maritime Organization’s (IMO) carbon intensity indicators (CII) are making older, less efficient tankers economically unviable.

- Strategic Fleet Renewal: Large-scale operators like Frontline and Euronav are not buying ships for today’s war; they are buying them because the current conflict provides the high freight rates (exceeding $100,000 per day in some cycles) necessary to fund the $120 million capital expenditure of a new Chinese-built VLCC.

The Cost Function of Tanker Construction

The economics of a newbuild tanker order are governed by three primary variables: the Steel Weight Ratio, the Propulsion Efficiency Quotient, and the Financing Cost Differential.

Steel Weight and Structural Integrity

Tankers are essentially floating steel envelopes. The cost of Grade A shipbuilding steel accounts for approximately 25-30% of the total contract price. China’s State Shipbuilding Corporation (CSSC) benefits from internal transfer pricing, allowing them to maintain margins even when global ore prices fluctuate.

Propulsion Efficiency Quotient (PEQ)

Modern Chinese-built tankers are focusing on "Eco-designs." A vessel delivered in 2026 will consume approximately 15% less fuel than a vessel delivered in 2014. In a high-oil-price environment—a direct byproduct of the Iran conflict—the PEQ becomes the single most important factor in a ship’s long-term Net Present Value (NPV).

Financing and Credit Lines

The Export-Import Bank of China (Chexim) provides aggressive financing terms. While Western banks have tightened lending due to Environmental, Social, and Governance (ESG) constraints regarding fossil fuel infrastructure, Chinese financial institutions view tanker construction as a strategic necessity. This creates a financing arbitrage where owners can secure lower interest rates in exchange for building in Chinese yards.

Risk Assessment of the Tanker Super-Cycle

The assumption that war-driven demand is a permanent floor for the market is a dangerous simplification. Several systemic risks could invert this logic:

- The Demand Destruction Threshold: If oil prices exceed $110-$120 per barrel due to a total blockade of the Strait of Hormuz, global consumption may contract. A drop in crude demand negates the ton-mile advantage of rerouting, leading to an oversupply of new hulls.

- Geopolitical Pivot: Should a diplomatic resolution occur, the "risk premium" vanishes. Ships ordered at peak-market prices (currently ~$128M for a VLCC) could become distressed assets before they are even launched.

- The Technology Trap: As the industry moves toward ammonia or hydrogen as fuel, the current generation of dual-fuel tankers may face accelerated depreciation. Chinese yards are proficient at current tech but remain in a secondary position regarding next-generation zero-emission R&D compared to Japanese specialized yards.

Strategic Positioning for Fleet Operators

The current environment demands an aggressive but calculated capital deployment. The optimal strategy for operators is to secure "early-berth" slots in second-tier Chinese yards that have recently undergone modernization. These yards offer the same structural designs as top-tier facilities but are currently pricing at a 5-8% discount to gain market share.

Operators must prioritize "scrubber-fitted" vessels despite the transition toward greener fuels. The spread between High Sulfur Fuel Oil (HSFO) and Very Low Sulfur Fuel Oil (VLSFO) remains wide enough that a scrubber—which cleans exhaust gases—pays for itself within 18 to 24 months during periods of high geopolitical volatility.

The shift toward Chinese shipyards is not a temporary anomaly but the culmination of a decade-long transfer of industrial competence. The conflict in the Middle East has merely acted as the catalyst that forced shipowners to accept the new reality: the future of energy transport is being forged in the drydocks of the Yangtze River delta, not the shipyards of Ulsan or Nagasaki. Operators who delay their replacement cycle in hopes of lower prices risk being squeezed out by the compounding effects of fleet aging and tightening environmental regulations. The tactical move is to lock in 2027 delivery slots now, before the next inevitable spike in regional instability further reduces the available global drydock footprint.