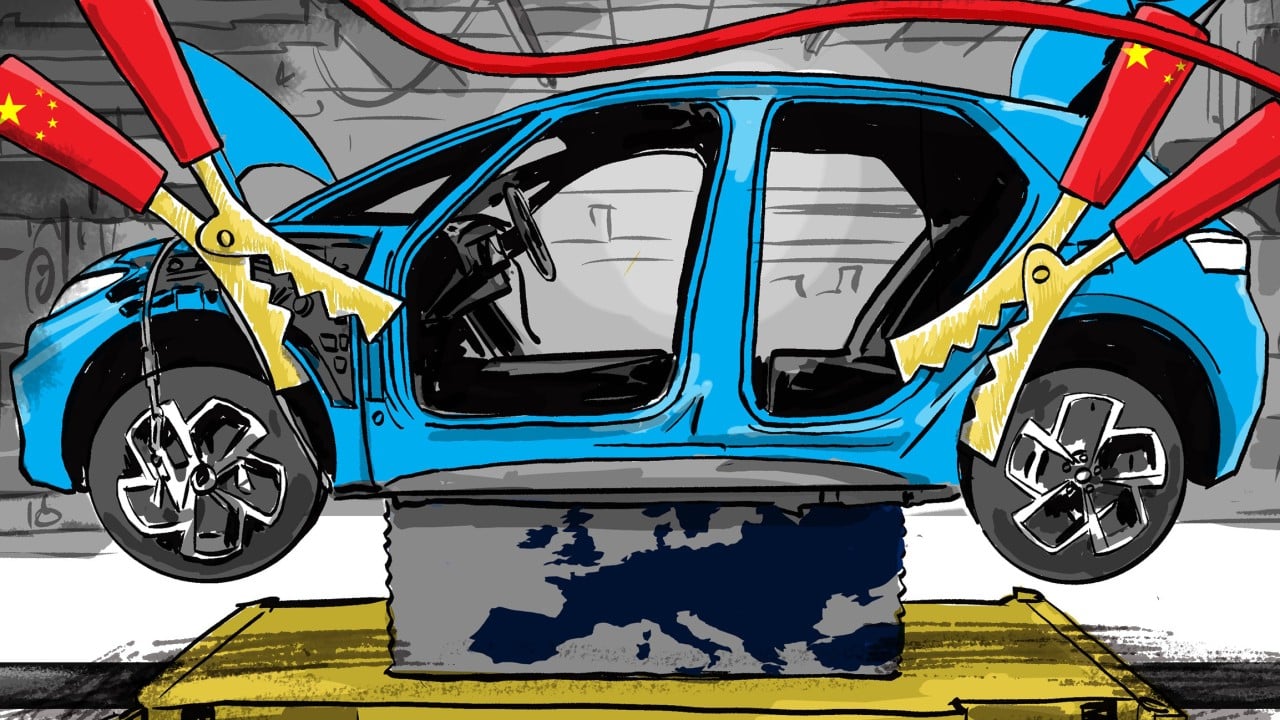

The narrative is comforting. It populates the pages of mainstream financial broadsheets and dominates the panel discussions at Zurich consensus conferences. The story goes like this: European automotive manufacturing is sluggish, bogged down by legacy supply chains and bureaucratic inertia. Suddenly, agile Chinese Electric Vehicle (EV) conglomerates arrive, establishing factories in Hungary and Poland, injecting capital, and teaching old dogs new tricks. They call it a revitalization.

They are wrong.

This is not a life raft for Europe’s auto industry. It is an execution method disguised as a partnership.

The belief that foreign manufacturing investment automatically elevates a domestic ecosystem relies on an outdated, 1980s understanding of globalization. When Toyota and Honda built plants in Ohio and Kentucky decades ago, they integrated into a local ecosystem, uplifting American tier-one suppliers. The current Chinese EV expansion into Europe operates on a fundamentally different blueprint. It is a vertically integrated, closed-loop system designed to extract value, hollow out local engineering capabilities, and reduce historic European brands to mere distribution networks.

The Localization Myth

The popular press loves a ribbon-cutting ceremony. When BYD announces a major manufacturing hub in Szeged, Hungary, or Chery targets production in Spain, commentators celebrate the local jobs created.

Let's look at the actual architecture of modern EV manufacturing. The value in a legacy internal combustion engine vehicle lived in the power train—the engine block, the transmission, the intricate machining. These were components European engineers mastered over a century, supporting a massive web of regional machine shops and specialized component makers.

In an electric vehicle, up to 40% of the bill of materials sits entirely within the battery pack, specifically the chemistry of the cells. The remaining value is concentrated in the power electronics and the software stack.

Chinese EV giants do not source these critical components from European suppliers. They bring their own. Contemporary Amperex Technology Co. Limited (CATL) and EVE Energy are already building their own massive battery facilities right next door to these new vehicle assembly plants. The high-margin, intellectually intensive work remains firmly tethered to R&D centers in Shenzhen, Shanghai, and Hangzhou.

Europe is getting the low-margin grunt work: final assembly, stamping sheet metal, and screwing panels together. This is assembly, not manufacturing.

Dismantling the Overcapacity Defense

Defenders of the current trajectory argue that European automakers need this competition to force efficiency. Volkswagen, Stellantis, and Renault have faced falling margins and utilization rates at their domestic plants. The theory suggests that the arrival of hyper-efficient Chinese production lines on European soil will catalyze a localized industrial renaissance.

This ignores the structural reality of state-directed capitalism. Chinese EV production capacity did not scale to its current heights merely through superior corporate strategy. It expanded via massive, systemic state subsidies, cheap land allocation, and state-backed bank loans that do not answer to traditional equity markets.

When a company operates with a mandate focused on market-share acquisition rather than immediate capital returns, standard market forces break down. European OEMs (Original Equipment Manufacturers) cannot cut costs fast enough to match a competitor whose supply chain is insulated from market-rate capital.

Consider the cost curve of lithium iron phosphate (LFP) batteries. Chinese manufacturers have locked down the refining capacity for battery-grade lithium, cobalt, and graphite. If a European legacy automaker attempts to source these materials independently to build a competing low-cost EV, they pay a premium. If they buy the finished battery packs from their Chinese counterparts, they hand over their margins and their strategic independence. It is a structural trap.

The Software Trait Shift

I have spent years analyzing the cost structures of industrial supply chains, watching Western executives convince themselves that manufacturing is just a commodity while they retain the "brand value."

We saw this play out in the consumer electronics sector during the 2000s. Western brands thought they could outsource the messy, low-margin business of building laptops and smartphones to Taiwanese and Chinese contract manufacturers while keeping the lucrative design work. Within a decade, those contract manufacturers developed their own engineering expertise, launched their own brands, and relegated their former clients to historical footnotes.

The automotive industry is repeating this mistake, but in reverse. European brands are attempting to preserve their prestigious badges while ceding the core technological architecture to foreign entities.

The modern premium vehicle is a smartphone on wheels. The value lies in the Advanced Driver Assistance Systems (ADAS), the over-the-air update capability, the infotainment ecosystem, and the thermal management algorithms. When European legacy brands enter joint ventures or allow foreign infrastructure to dominate their domestic turf, they lose the data feedback loop.

A vehicle running on a foreign-designed computing platform sends data back to the cloud that designed it. That data trains the next generation of machine learning models, refines the autonomous driving algorithms, and optimizes battery degradation models. The domestic industry is cut out of the intellectual compound interest that drives modern technological development.

The Threat to Tier-Two and Tier-Three Suppliers

While the public focuses on the logos on the front of the cars, the real carnage will happen three steps down the supply chain. Europe’s true industrial backbone isn’t Volkswagen or BMW; it is the thousands of mid-sized, often family-owned, tier-two and tier-three suppliers across Germany, northern Italy, and France.

These companies produce the high-precision valves, the specialized gearboxes, and the fuel-injection systems that defined automotive excellence for generations. They employ millions of highly skilled, highly paid workers.

A Chinese EV requires a fraction of the moving parts of an internal combustion vehicle. The components it does require—electric motors, inverters, sensors—are highly standardized and produced at a scale in Asia that no European mid-sized supplier can match.

When Chinese OEMs build vehicles in Europe, they do not integrate these regional suppliers. They bring a pre-packaged, pre-vetted network of component suppliers with them. The domestic tier-two and tier-three ecosystem faces a sudden, catastrophic demand cliff. Without a customer base to fund their own transition to EV component manufacturing, these specialized engineering firms will collapse. Once that industrial knowledge base dissolves, it cannot be rebuilt by passing a tariff or signing a political accord.

The Flawed Premise of Trade Protectionism

The standard policy response to this structural shift has been the implementation of import tariffs. The European Commission's anti-subsidy investigation and subsequent tariffs on Chinese-built EVs were heralded as a victory for domestic industry.

This policy response misunderstands the agility of modern industrial capital. Tariffs only work if they target a fixed manufacturing point. By establishing factories directly inside the European customs union—whether in Hungary, Spain, or through partnerships in non-EU states like Turkey—Chinese automakers completely bypass the tariff wall.

Even worse, the threat of tariffs accelerates the timeline for localization. Instead of exporting finished vehicles from Shanghai, these companies are building highly automated factories inside Europe ahead of schedule. Because these factories leverage advanced automation and pre-assembled component kits imported from Asia, they require far fewer workers per vehicle than traditional European plants.

The result? The tariffs do not protect European jobs. They simply force the replacement of European-engineered vehicles with foreign-engineered vehicles built within Europe's own borders.

The Hard Truth for European Automotive Strategy

Legacy automotive boards like to talk about their heritage, their design prowess, and their ride-handling dynamics. They believe a consumer will always pay a premium for a badge with a century of history behind it.

That assumption holds true for ultra-luxury vehicles, but it fails completely in the mass-market and volume premium segments. The next generation of car buyers does not care about the mechanical feel of a steering column or the traditional prestige of a heritage brand. They care about software integration, interior digital real estate, charging speeds, and price-to-range ratios.

In these categories, the gap is not closing; it is widening.

If European automakers want to survive, they must stop looking for salvation in joint ventures, real estate deals, and local manufacturing mandates. They need to abandon the delusion that foreign capital arriving on their shores is a sign of industrial health.

The only viable path forward is an aggressive, coordinated decoupling from the established battery supply chain. It requires massive, high-risk capital allocation into next-generation solid-state battery chemistry, radical vertical integration of software development, and the painful, immediate retirement of legacy internal combustion assets.

Every Euro spent trying to prolong the life of a diesel platform or negotiating a manufacturing partnership with an incoming competitor is capital diverted from the actual survival fight. The factory gates are opening, the production lines are turning on, and the old guard is smiling for the cameras at the opening ceremonies of their own obsolescence. Stop celebrating the investment. The siege is already over, and the occupying force is just moving into the castle.